Should You Select a Target Date Fund or Mutual Funds in Your 401(k)?

Choosing the right investment strategy for your 401(k) is a crucial decision that can significantly impact your retirement savings. Two popular options are Target Date Funds (TDFs) and Mutual Funds. Each has its unique advantages and disadvantages. In this blog post, we'll explore the pros and cons of both to help you make an informed decision.

What Are Target Date Funds?

Target Date Funds are designed to simplify retirement investing. They automatically adjust their asset allocation—mix of stocks, bonds, and other investments—based on a specific target retirement date. As the target date approaches, the fund gradually shifts from a growth-oriented strategy to a more conservative approach.

Pros of Target Date Funds

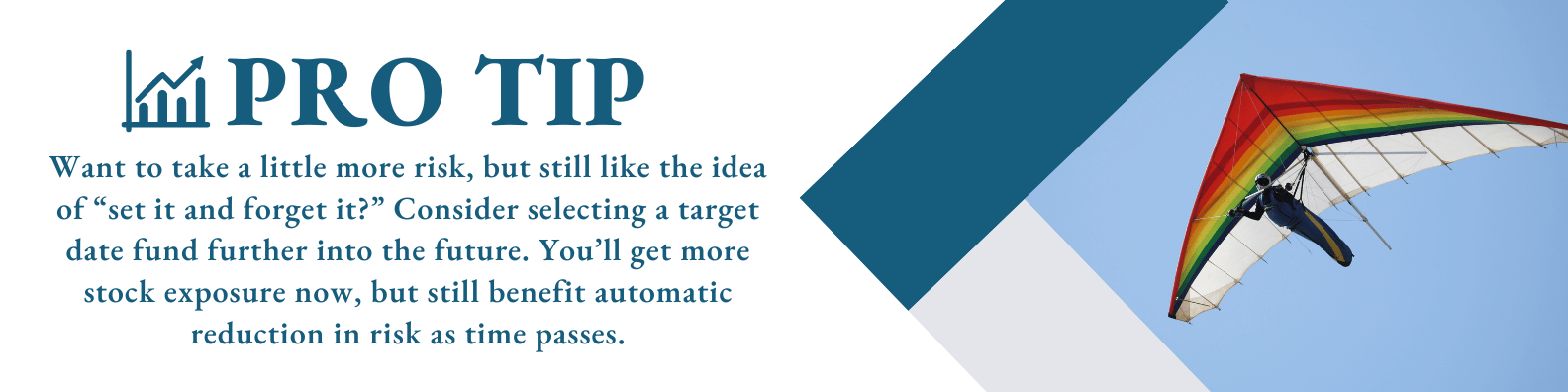

Simplicity and Convenience: TDFs offer a hands-off approach to investing. Once you choose a fund with a target date closest to your retirement year, the fund manager takes care of the rest.

Automatic Rebalancing: TDFs automatically rebalance their portfolios to become more conservative as you near retirement, reducing the risk of significant losses.

Diversification: These funds typically invest in a mix of asset classes, providing built-in diversification.

Cons of Target Date Funds

One-Size-Fits-All Approach: TDFs may not account for your individual risk tolerance, financial goals, or changing circumstances.

Fees: Some TDFs can have higher expense ratios compared to other investment options, potentially eating into your returns.

Performance Variability: Not all TDFs perform equally, and some may underperform compared to a well-managed, custom portfolio.

What Are Mutual Funds?

Mutual Funds pool money from multiple investors to purchase a diversified portfolio of stocks, bonds, or other securities. Investors buy shares in the mutual fund, and the fund is managed by professional portfolio managers.

Pros of Mutual Funds

Customization: You can tailor your investment strategy by selecting mutual funds that match your risk tolerance, financial goals, and investment preferences.

Variety: With thousands of mutual funds available, you can choose from a wide range of asset classes, sectors, and investment styles.

Active Management: Many mutual funds are actively managed, meaning professional managers make strategic decisions to maximize returns and minimize risks.

Cons of Mutual Funds

Complexity: Building and managing a diversified portfolio of mutual funds requires time, knowledge, and regular monitoring.

Fees: Actively managed mutual funds often have higher fees compared to passively managed funds, which can impact your net returns.

Risk of Underperformance: Actively managed funds may underperform their benchmark indices, especially after accounting for fees.

Which Should You Choose?

The choice between Target Date Funds and Mutual Funds depends on your individual needs, preferences, and investment strategy.

Choose Target Date Funds if:

You prefer a simple, hands-off investment approach.

You want automatic rebalancing as you approach retirement.

You seek a diversified portfolio without having to manage it actively.

Choose Mutual Funds if:

You want more control over your investment choices.

You are willing to spend time researching and managing your portfolio.

You seek potentially higher returns through active management and customization.

Conclusion

Both Target Date Funds and Mutual Funds offer valuable benefits for your 401(k). TDFs provide a convenient, set-it-and-forget-it solution, while mutual funds offer flexibility and potential for customization. Carefully consider your financial goals, risk tolerance, and investment knowledge before making a decision. Consulting with a financial advisor can also help tailor an investment strategy that best fits your retirement objectives.